From 100 to 5,000 Paying Customers in 2 Years: The Attio Teardown

Strategy behind 10x first-year growth. Infrastructure that became distribution. Founder mindset that cracked a mature $63B market.

In this analysis you’ll learn:

The mechanics behind 10x growth after 1st year of public launch

The Vertical Trap - when niche traction masks a market ceiling

PLG & Product-led sales strategies in action

Company culture behind a product people love

How hard things become a Deferred Lever

Strategic Summary: Attio is the fastest-growing CRM in 2026. The company started as Fundstack, a vertical CRM for venture capital firms, before pivoting in 2019 to attack the $63B CRM market dominated by Salesforce and HubSpot. The defining decision was spending 3+ years building a new data architecture from scratch before going public. This architectural advantage translates directly into distribution: templates install in 30 seconds, onboarding delivers value in under 3 minutes, and migration from competitors takes hours instead of months. Attio reached $1M ARR before public launch, grew from ~100 to 1,000 paying customers in the first year, and scaled to 5,000 paying customers within 2 years by Series B ($116M raised total, led by GV). The go-to-market engine combines product-led growth (75% organic signups) with Product-Led Sales - the product enters bottom-up through builders and operators, then sales converts scattered adoption into company-wide contracts.

The beginning

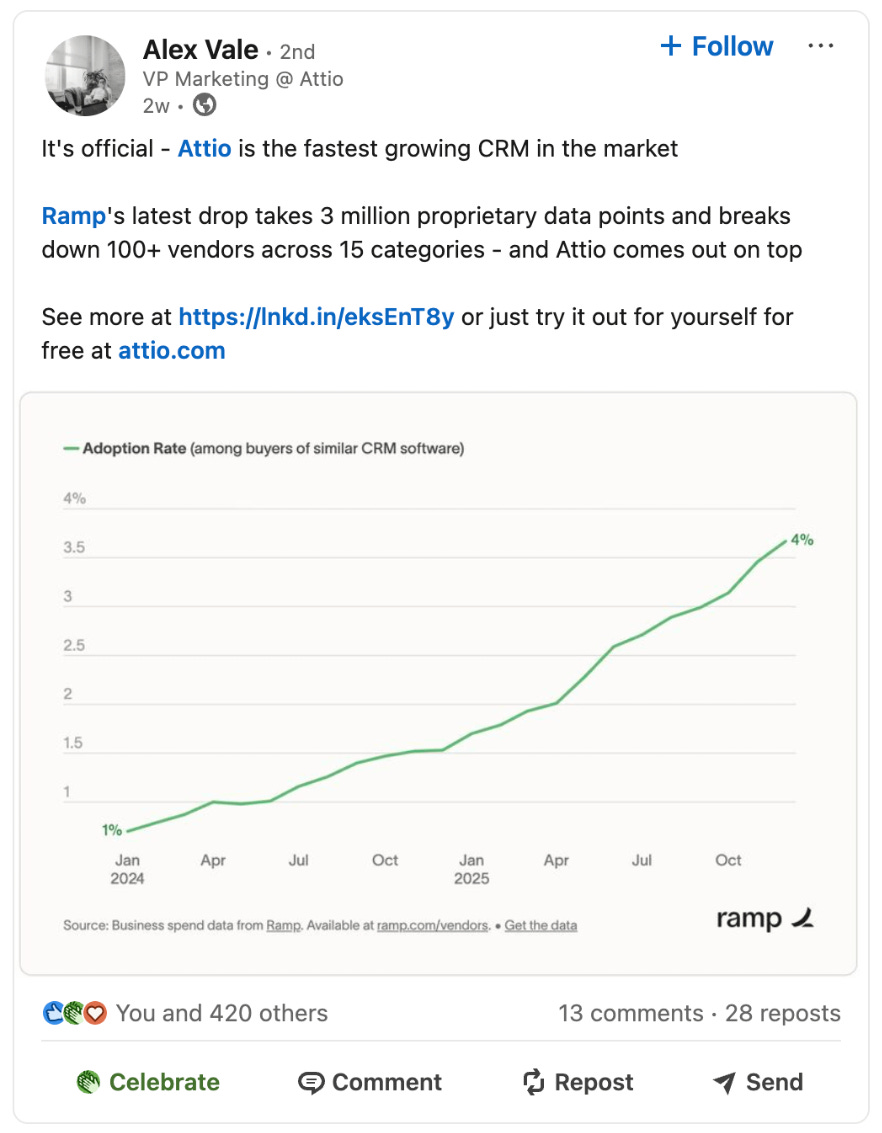

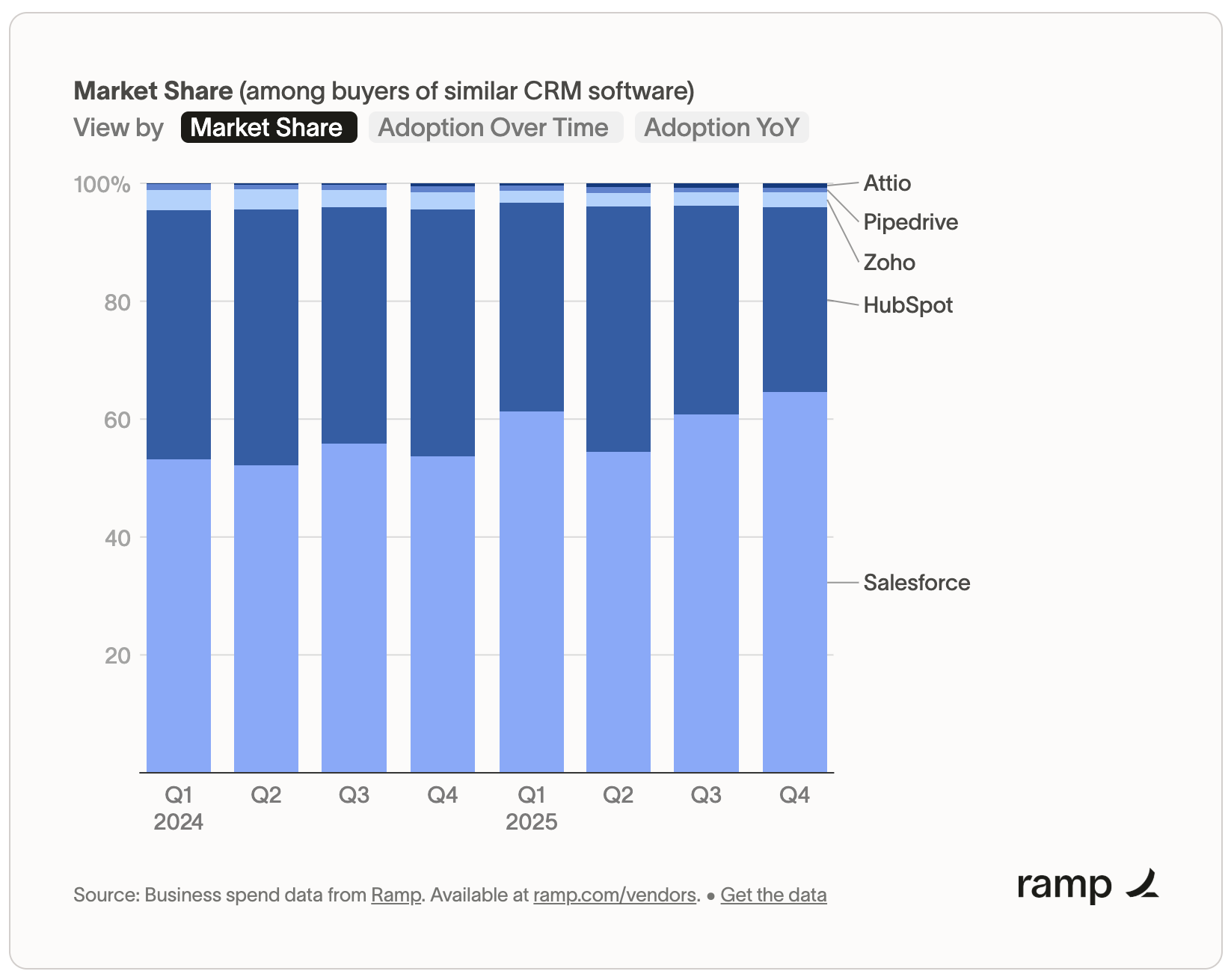

Within two years of public launch, Attio captured ~4% adoption among CRM users and reached #5 in the category - behind Salesforce, HubSpot, Pipedrive, and Zoho. Confirmed by Ramp’s January 2026 vendor analysis across 3 million data points. Strongest traction is in micro-SMB (6% adoption), tapering to ~1% in mid-market and enterprise. The trajectory - from zero market presence to top five in 24 months - is the result of great software and years of building credibility before going public.

The Vertical Trap

The story starts in 2017 with a company called Fundstack.

Nicolas Sharp and Alexander Christie were building inside the venture capital world when they spotted a fundamental problem. VCs received hundreds of emails, calendar invites, and meeting requests daily. Relationships were getting lost in the noise.

Fundstack solved this by automatically building a user’s network from their email data. Connect your inbox, and the system aggregated, enriched, and organized every contact you’d ever interacted with. For the VC community, it worked. The product generated revenue. It had real traction.

But two years in, the founders hit a ceiling they couldn’t engineer around. The VC and private equity market was too small to sustain what they actually wanted to build.

The Vertical Trap. It says start with a niche and it’s correct. A sharp problem, a clear audience, a defined ICP. But the niche must have room to expand. If the market ceiling is too low, traction becomes a trap: the product works, but the business can’t scale. This is why sizing the total addressable market matters before committing.

Attio’s case mirrors Sword Health. Sword started with limb paralysis patients - a real but extremely narrow group - then expanded to the broader MSK physiotherapy market. Both pivots took roughly two years of building before the founders recognized the ceiling. Both required starting nearly from scratch. The pattern: the original problem was valid, but the original market was a cage.

The Larva Phase

After the pivot, Attio entered the larva phase - direction found, but the company still had a long way to scale. From 2019 to late 2022, full focus on the project for three years in the dark.

They entered the $63B market owned by Salesforce and HubSpot for over 15 years. It was mature, crowded and seemingly settled. But the founders saw what incumbents couldn’t admit - their infrastructure was aging, and no amount of feature layering could fix a rigid foundation. The gap was wide enough for the ‘10x better’ rule to apply.

The bet followed a counterintuitive principle: hard things make everything else easier - this is a deferred lever. It doesn’t activate on day one. Hard projects are a nightmare before they’re a magnet - the shift happens when results start proving the vision. Sword Health, Figma, Gmail followed the same arc. Then difficulty itself becomes the attractor for talent, capital, and customers.

The dark period hit hard. Sharp described it openly: “There were so many times we wanted to give up. Day after day the feeling was, ‘This is a disaster.’ We’ve interviewed 400 engineers and no one wants to work with us.” His survival framework was one question: “If you were to start again, is this a company you would start again?” The answer was always yes. So they kept building - from scratch, for over three years. Similar to how Google spent 4 years developing Gmail before launch, Attio chose to rebuild the foundation on new technology.

4 pillars of great product

The product rested on four pillars:

Flexible Data Model. Traditional CRMs force users into rigid pipelines - fixed fields, fixed stages, fixed logic. Attio lets teams define custom objects that mirror how their business actually works as a basic feature. Sales pipelines, renewal tracking, churn monitoring, revenue expansion - all configurable without developers or consultants. The system adapts to the company, not the other way around.

Automatic Data Enrichment - inherited from Fundstack’s DNA. Attio instantly builds a populated CRM with every person and company you’ve ever interacted with through Gmail and calendar integration. CTO Christie set the onboarding target: time-to-value under 3 minutes.

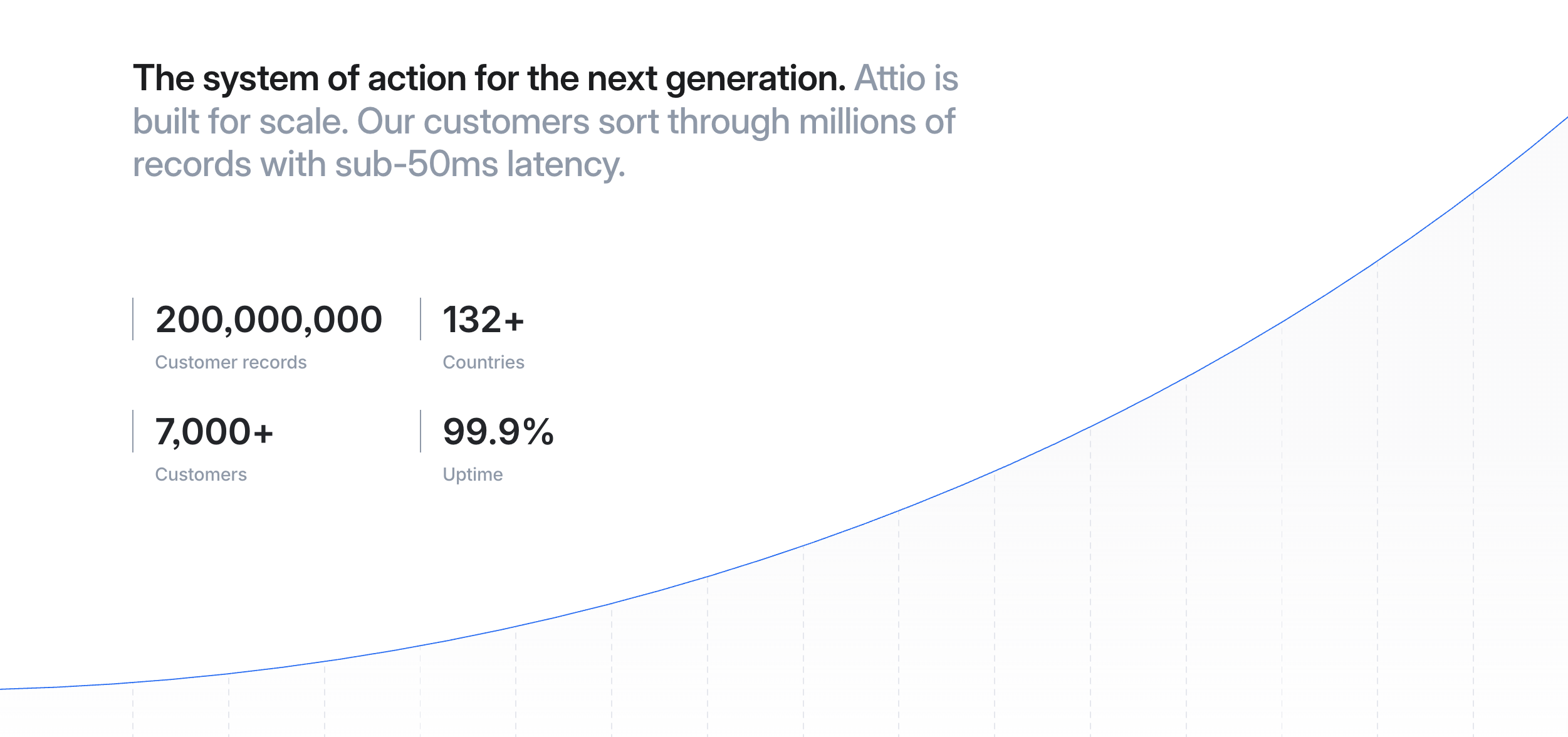

AI-Native Architecture. They built for AI from the ground up - a three-layer structure: a system of record (custom objects at sub-50ms latency), a system of context (automatic ingestion of emails, calls, documents), and a system of action (AI agents executing GTM tasks that previously required human judgment).

Modern UX. Consistently described as “the first CRM that feels truly modern.” Real-time multiplayer collaboration, command-K launcher, near-zero-latency search - conventions borrowed from Notion and Google Sheets. If you’re comfortable in those tools, Attio feels native.

Product development

Attio built the product the way lean startups are supposed to - but rarely do. The process followed a clear sequence: do it manually, find the pattern, then encode it into software.

In the earliest phase, Sharp and the team onboarded every customer by hand. Manual data migration, custom workspace setups, hours spent watching users click through the product. The goal was pattern recognition. Which steps led to the “aha” moment? Where did users get stuck? What made them invite teammates? What made them leave?

Once the pattern repeated, they coded it. Guided workspace setup, opinionated templates, prompts to connect email and calendar early. The manual playbook became the product. Classic lean startup logic - but applied to the onboarding experience itself, not just the feature set.

The product loop they discovered was simple:

sign-up → connect data → see value → invite team → expand seats.

Every element of the onboarding was tuned to push users through this sequence as fast as possible. One critical insight shaped the design: Attio only sticks as a multiplayer tool. A single user gets value. A team gets locked in.

They also use Attio to track their own customers through the adoption journey. Trial expiries, seat spikes, downgrades - all routed through their own CRM to trigger sales or CS interventions. The product was simultaneously the thing they sold and the tool they used to sell it.

Monetization followed the same bottom-up logic. Attio iterated toward a reverse-trial model: new users start with full features, then choose to pay or fall back to free. Individual users enter at zero cost. Teams experience the full power together. Accounts expand naturally as seat count grows - no top-down negotiation required - at least not yet.

Do things that don’t scale - then scale the things that worked. Attio’s PLG engine wasn’t designed in a boardroom. It was discovered through hundreds of manual onboarding sessions where founders did the work themselves. The playbook came from observation, not theory. Once the pattern was clear - which actions led to activation, which led to expansion, which led to churn - they encoded it into software and removed themselves from the loop.

Product as Distribution

In a traditional CRM, the path to revenue looks like this:

sales call → signed contract → 3 months of implementation by consultants.

HubSpot and Salesforce need entire partner ecosystems just to get customers operational. The product doesn’t sell itself - an army of intermediaries sells it.

Attio’s architecture inverted this. Three mechanics turned the product into its own distribution channel:

Templates as entry points. Attio offers a library of pre-built workflows - fundraising pipelines, sales tracking, talent acquisition. A user installs a complete workflow in 30 seconds. For teams migrating from legacy CRMs, the same flexibility compresses a 3-month implementation into hours.

Land where legacy fails. Most companies use Salesforce for core sales - but processes like partnerships, investments, or customer success end up in Notion or Airtable because Salesforce is too rigid. Attio enters through these gaps. One team builds a workflow for one process, proves the value, then spreads across the organization.

API-first as developer advocacy. For most CRMs, the API is an afterthought. For Attio, it’s a primary distribution channel. Real-time data sync, clean documentation, modern architecture. When a developer needs to connect a CRM to their product’s data, Attio wins by default - it works like modern software. Developers become internal ambassadors who sell Attio to the rest of the company.

Infrastructure is distribution. Legacy CRMs are pre-assembled furniture - you get what’s in the box. Attio is Lego. Same bricks, infinite configurations. Every architectural decision - flexible data model, auto-enrichment, modern UX - compresses the distance between “signup” and “paying customer”.

Early-stage marketing

In their first years, go-to-market and product development were the same thing. By December 2022 - before any public launch Attio had crossed $1M ARR.

Three moves, executed during the larva phase:

Building in public. The founders shared code snippets, design decisions, and product thinking on X.com (Twitter) throughout the build period. This attracted a specific audience: builders and operators who tolerated an MVP-level product in exchange for shaping what it became. Sharp described the target: people who would “be a patient and forgiving tester for you.”

Founder-led sales. Sharp personally prospected on Reddit, X, and startup communities, then onboarded each customer by hand. Some setups took days - manual data migration, custom configurations, bespoke workarounds. Painful and unscalable. But every session was a discovery loop: mapping which steps led to the “aha” moment and what a modern CRM actually needed to do day-to-day.

Velvet rope strategy. Pre-2023, Attio ran a private beta with a waitlist of several thousand teams, onboarding selectively. Growth came from inbound interest, word-of-mouth, and VC connections - not outbound.

VC referral loop. Fundstack’s original customer base - venture capitalists - became Attio’s first organic distribution channel. VCs who used the tool recommended it to portfolio companies, creating one of the earliest sources of paying customers.

The founders invested in their own PR and proof-building from the start, treating public credibility as a compounding asset, not a launch-day tactic. By autumn 2020, they started collecting positive mentions appearing on X - including from TechCrunch.

The Velvet Rope. Most startups rush to open the gates. Attio did the opposite - they controlled access, charged premium prices, and used every customer as a research subject. The waitlist wasn’t a growth hack. It was a filter. Only users who matched the builder persona got in, which meant every feedback loop improved the product for the exact ICP they planned to scale with.

The Butterfly Phase

After three years in the dark, Attio launched publicly in March 2023. The decision was triggered by the convergence of signals that told the founders the product was ready.

The launch conditions:

Technical readiness. In the earliest beta, email sync took 3.5 days to complete, by launch, it happened in seconds. CTO Christie treated data freshness as the killer feature: the moment someone connects their email, insights must surface immediately. The infrastructure had to be invisible. If users noticed the technology, the technology wasn’t ready.

Retention signal. The DAU/MAU ratio reached a level the founders considered sufficient for a daily-use product.

Willingness to pay. Attio tested pricing early at a relatively high price point, and people paid. When they cut the price in half - close rates jumped. By the seed round (November 2021), they had 120 paying customers, $1M+ ARR.

Competitive pressure. New CRM competitors were appearing. Real-time data, flexible objects, modern UX - features Attio’s beta users validated daily - were becoming common. The window to establish category leadership was narrowing. Sharp recognized: “You can’t just build the best product, you also need to win the market”.

A hard deadline. The team set a company-wide launch date and committed to it collectively. It helped them avoid improving the tool endlessly.

Most startups launch too early - trying to scale before retention holds - or too late, after the window closes and unique advantages become table stakes. Attio timed it by stacking signals: retention held, users paid, the market was moving. The final accelerator was a hard deadline that aligned the entire company on a single date. Sharp now treats deadlines as a core operating tool: “Deadlines set the tempo and get people energized.”

Marketing tactics

The public launch in March 2023 was paired with a PR wave, a $23.5M Series A announcement covered by TechCrunch, and a #1 Product Hunt campaign - all timed to hit simultaneously, creating immediate momentum. The message was clear: Attio is no longer a private beta. It’s open, funded, and ready to compete.

As a result, 75% of signups came through organic channels. But the foundation of marketing was the product itself - the <3-minute onboarding that auto-syncs email and calendar data, instantly populating a CRM with enriched contacts. VP of Marketing Alex Vale called it the “magic moment.” Everything else was built to drive users toward that first experience.

They scaled marketing in layers - though some started years before launch. Vale described the full sequence: “Word of mouth from VCs, spreading to startups, building in public on social media, paid search, and eventually, organic social and broader word-of-mouth growth.”

Owned audience. Throughout the pre-launch build period, Attio invested in social presence, podcasts, and newsletters - building an audience before having a product to sell. By launch day, this wasn’t a cold start. Thousands of people already followed the journey and waited for access. This compounding exposure was likely one of the key factors behind Attio’s growth from ~100 paying customers at launch to over 1,000 within the first year.

Product Hunt as launchpad. Attio hit #1 on launch day. For a tool targeting builders and operators, Product Hunt delivered the right audience at the right moment - early adopters tracking innovation, ready to try a new CRM on the spot.

Paid channel. CRM is a high-intent category. People searching “CRM for startups” or “Salesforce alternative” are actively buying. Vale confirmed paid search was one of the earliest successful paid channels: “Paid search worked well in the early stages, helping build a pipeline of high-intent, qualified leads.”

Creator partnerships. In February 2025, Attio formally launched a selective Creator Partner Program targeting GTM leaders and B2B content creators - after running it informally with a few creators earlier. Benefits include free Pro workspace, early feature access, ad spend support, and direct access to the product team. The program is invite-only. Attio recently hired a dedicated Creator Partnerships Lead, signaling this is a strategic channel for 2025-2026, not an experiment.

Sales strategy

Attio’s ICP isn’t the VP of Sales. It’s the builder - the operator, the RevOps lead, the technical founder who configures tools themselves and shows the team. This is bottom-up distribution - one person adopts, the team follows.

The product sells first. Free plan, 14-day trial, self-serve signup - small teams adopt Attio without ever talking to sales. The product handles acquisition. This shifted the sales team’s center of gravity: instead of cold outreach, they focus on helping new users design their workspace, configure workflows, and expand usage. The sales team doesn’t generate demand. It converts demand that the product and marketing already created.

To scale this further, they run Product-Led Sales. When someone creates a workspace, connects their API, and invites colleagues - the sales team receives a signal to reach out to the decision makers. They have context to say: “Hey, your ops team is already building on Attio. Let’s help you roll this out globally.”

The product opens the door. Sales walks through it. But this matters most at scale. Attio’s bottom-up approach works - until the CFO asks why five teams pay separately for tools that do the same thing. The sales team needs to convert scattered adoption into one company-wide contract before that question triggers top-down consolidation.

The Trojan Horse. Legacy CRM sales start at the front gate - pitch the CEO, negotiate the contract, deploy consultants. Attio enters through the side door as “a small tool for the RevOps team.” By the time the license renewal comes around, critical workflows, customer data, and institutional knowledge already live inside Attio. The switching cost is no longer price - it’s operational disruption. Salesforce wins deals top-down. Attio wins bottom-up with sales support.

Growth Milestones

Attio crossed $1M ARR in December 2022 with ~100 paying companies - still in private beta. Three months later, the public launch paired with a Series A announcement revealed the full scale: 2,000+ customers across 100+ countries, most on free or trial tiers.

Product Culture & Organizational DNA

Product and marketing matter - but so does the company mindset that turns vision into a working product the market actually needs. Attio’s founders built their organization around a few principles they publicly credit for the product’s shape and success:

Product engineers, not software engineers. Attio doesn’t hire coders who wait for specs. Every engineer is a product engineer - they design, build, test, and validate features end-to-end. This model allowed Attio to operate without a single product manager for nearly 7 years. The first PM was hired around 2024. Sharp and Christie modeled the approach after early GitHub and Stripe. The result: fewer people, faster decisions, and a product built by people who understand both the code and the customer.

Context over control. Founders handle the 50% that shapes direction - data architecture, platform strategy, AI vision. The other 50% - features driven by customer feedback, UX improvements, workflow fixes - is executed autonomously by the team without heavy top-down approval. If a customer reports friction, the engineer closest to the problem fixes it, tests it, and ships it. This split keeps the product both ambitious and responsive. The 50/50 split isn’t a documented KPI - it’s how they describe their prioritization philosophy.

Company-wide deadlines Sharp discovered during the launch push that hard deadlines work - they set the tempo and get people energized. Attio now uses them as a core operating tool across the company.

Democratized features. Most legacy CRMs gate powerful features behind enterprise pricing. Attio pushes significantly more power into lower plans - strong automation, flexible data model, and API access on self-serve tiers. Full custom objects unlock at Pro, not Enterprise. The heaviest gating - SSO, dedicated CSM, advanced permissions - is reserved for organizational needs, not core functionality. The logic: the more people who use the tool, the stronger the lock-in. Sharp confirmed: CRM’s value “comes from the number of team members using it… you don’t want it to just be used by a few power users.” Monetization follows seat expansion and usage, not feature paywalls.

Funding

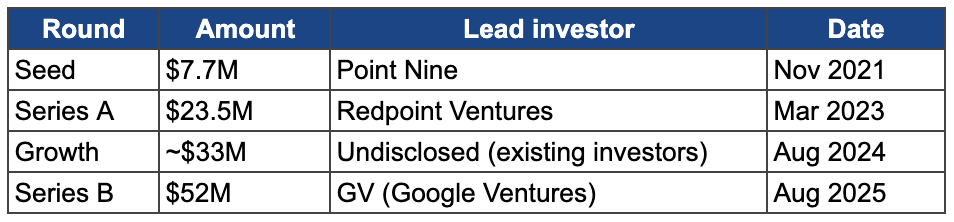

Total raised: $116M - each round funded a different phase - but the priority never changed: product first, distribution second.

Seed funded the larva phase. Four years of building with a small team, no “mainstream” marketing or sales. The $7.7M bought time to build Particle and run the private beta.

Series A ($23.5M + growth ~$33M) coincided with a public launch. Attio earmarked funds to expand the Particle data layer for more complex workflows, accelerate product development including AI features and integrations, and grow GTM presence globally - with emphasis on US and Europe. Engineering and product took the larger share. GTM was explicit but secondary.

Series B ($52M) shifted the narrative to “AI-native CRM.” Attio committed to scaling heavy R&D to ship faster, with focus areas including agent collaboration, granular permissions, and predictive intelligence. Product development priorities: native data ingestion, intelligent workflows, and programmable surfaces (APIs, App SDK). The marketing engine scales in parallel - more regions, more support - but the investment thesis remains product-led: deepen the moat, then distribute.

GV as Series B lead likely isn’t accidental. Google Ventures leading a $52M round for a company built on Google Cloud infrastructure signals strategic alignment beyond financial return. Attio’s architecture runs on the same ecosystem GV’s parent company sells. When your lead investor also provides your core infrastructure, the relationship compounds in both directions - credibility for Attio, ecosystem validation for Google Cloud.

Key Takeaways

1. Infrastructure decisions are distribution decisions. Most founders treat technology as a backend choice and distribution as a frontend problem. Attio proved they’re the same decision. Cloud Spanner wasn’t picked just for performance - it was picked as a foundation of product-led growth - the product should be flexible and meet custom user needs immediately. If your tech stack creates friction in adoption, you don’t have a marketing problem - you have an infrastructure problem.

2. Choosing a small market could be your golden cage. Fundstack had revenue, retention, and happy customers. It still wasn’t a business worth building. The Vertical Trap is dangerous precisely because it looks like success - all the metrics are green, but the ceiling is invisible until you hit it. Before committing years to a niche, size the market. Revenue validates the problem. Market size validates the business.

3. Manual before automated. Attio’s PLG engine - the onboarding flow, the activation triggers, the expansion loops - wasn’t designed. It was discovered through hundreds of manual sessions where founders watched users click, struggle, and leave. The pattern came first. The code came second. Most startups automate assumptions. Attio automated observations. The difference is the reason their onboarding is fast and their user experience is strong.

4. Controlled access beats open access in the build phase. The velvet rope strategy - selective beta, premium pricing, curated users - gave Attio something regular customer acquisition never could: a product shaped by its ideal customer and a controlled feedback loop through cohort-based access. Opening the gates early feels like progress, but it often brings noise and early churn.

5. Hard things are a deferred lever - not a default one. Choosing the harder market, the harder technology, the harder problem doesn’t pay off immediately. It’s a nightmare before it’s a magnet. But when results start proving the vision, the difficulty itself attracts talent, capital, and customers. The key word is “deferred.” Most founders quit before this lever activates.

6. Launch timing is signal stacking, not gut feeling. Attio didn’t launch when the product felt ready. They launched when five independent signals converged: technical stability, retention, willingness to pay, competitive pressure, and a hard deadline. Launching on hope kills startups fast. Attio proved the alternative: stack signals, control entry, commit when the data converges.

“If you were to start again, is this a company you would start again?”

Nicolas Sharp, co-founder Attio

Thanks for your time!

Kasper