From 50 Rejections to $4B: The Sword Health Teardown

Strategy behind 600% YoY growth. Levers reaching millions of patients. Brave pivots that turned rejection into dominance.

In this analysis, you’ll learn:

The pricing mechanics and sales strategy behind 600% YoY growth.

Healthcare “traps” that look like product-market fit failures.

Distribution levers that unlock access to millions of patients.

How Sword optimized revenue through: distribution and product.

The AI shift that increased patient-serving capacity by 7-17x per therapist.

Two strategic moves that could define Sword’s next growth phase.

Strategic Summary: Sword Health built a $4B company by following first principles - not patients, but whoever pays for them. They avoided the B2C trap, bypassed the Provider trap, and sold directly to US employers who pay for employees’ MSK treatment. Capital efficiency (10.5x vs Hinge’s 2.4x) came from forced scarcity, not VC abundance. Phoenix AI delivers 7-17x therapist efficiency. Reverse M&A buys distribution, not technology. 100% client retention comes from pricing model and superior products. They’re now positioned to capture Europe through “Payvider” partnerships and the emerging senior care market.

Why Sword Health?

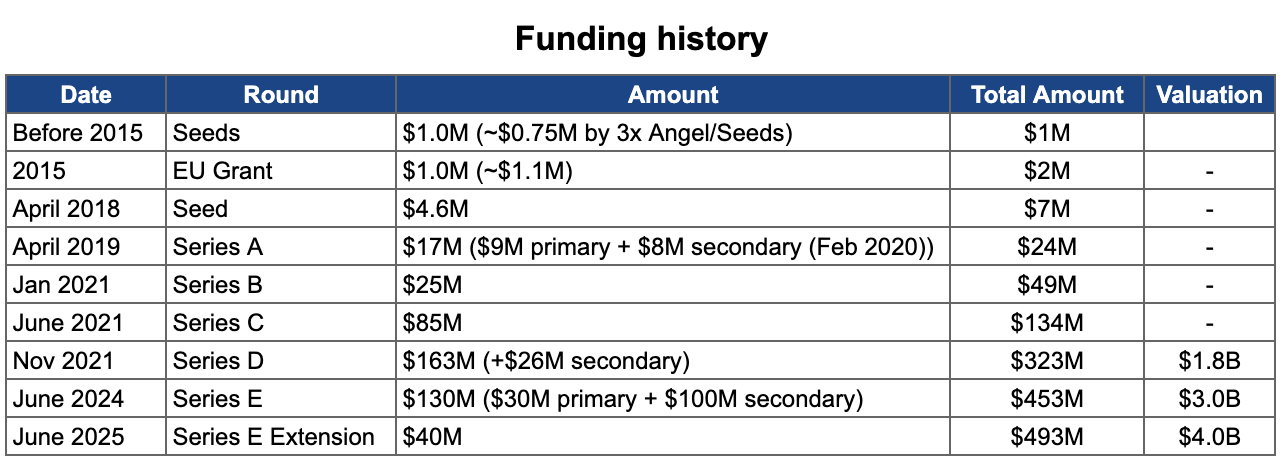

Sword Health got 50 rejections from European VCs. Four weeks after one cold email to Khosla, they closed $17M. Five years later: $4B valuation, zero client churn, and they just acquired one of their biggest competitors.

1.7B people suffer from musculoskeletal pain. Treatment is expensive, rehabilitation takes time, effort, and money. What makes it worse - many patients could avoid surgery or serious health consequences if they chose prevention earlier.

The CEO, Virgilio Bento, was 10 years old when his brother suffered an accident and spent 12 years recovering from a one-year coma. Virgilio watched his parents struggle to find the best PT (physical therapist) and saw how much money and time they spent. He decided to change the way people like his brother recover.

Sword Health has the potential to become the US and EU industry leader.

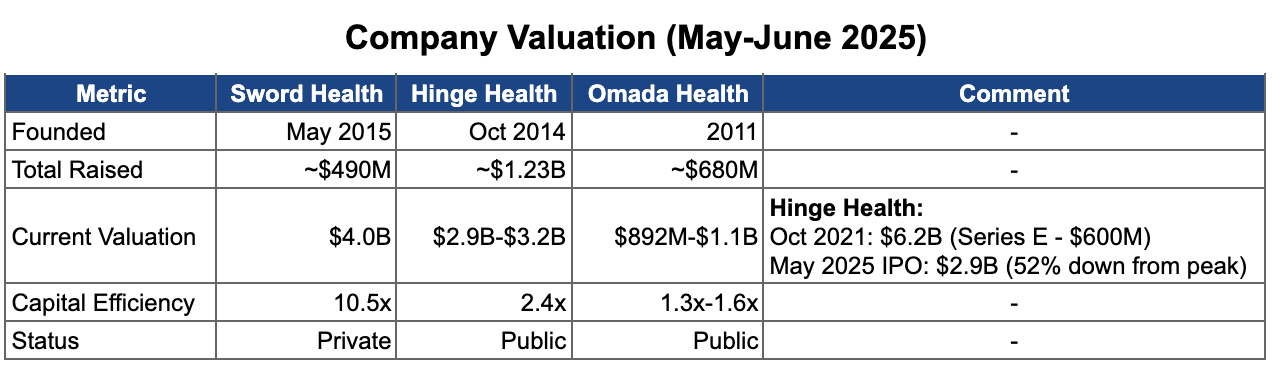

💡 Sword raised $490M vs Hinge Health’s $1.23B - yet achieved a higher valuation ($4B vs $2.9B). Capital efficiency ratio: 10.5x vs 2.4x. Sword’s 4-year “larva phase” of forced scarcity built operational discipline that venture-funded competitors never developed. Hinge could afford inefficiency. Sword couldn’t, and that constraint became their advantage.

The beginning

Bento started the company in Portugal, building on his PhD research (2009-2013), alongside co-founder Márcio Colunas. They set out to create digital therapy to help people with limb paralysis at home.

Before significant private capital was available, they relied on a €1 million EU research grant in 2014 to survive the deep R&D phase.

In 2015, they officially launched SWORD (an acronym for “Stroke Wearable Operative Rehabilitation Device”) and entered a four-year period of extended R&D where financing was extremely difficult.

Beyond the grant, they relied on small seed investments of $100,000, $250,000, and $400,000. Barely enough to sustain operations, let alone scale - forcing the company to operate lean while perfecting its sensor technology and AI.

In the early years, Sword attempted to sell to hospitals and rehabilitation centers. This strategy failed because providers viewed the technology as a disruption to their workflows and resisted digital-first models.

💡Portugal was not Silicon Valley - healthcare is very risky for most VCs. A 2014 seed round would have cost 20-30% equity for maybe $1-2M. The EU grant gave them €1M for 0% dilution. That single decision compounded: when Khosla wrote the $17M Series A check in Feb 2020, founders likely still controlled the cap table.

The “Larva” phase

Between 2015 and 2019, Sword remained in extended R&D mode to perfect their technology. Even though competitors grew and money was tight, Sword chose patience over premature scaling.

While Sword was on hold, their competitors walked into the B2C trap.

Hinge, Kaia, and Omada - when collaboration with clinics failed - tried to pivot from hospitals to treating patients at home. Their product gained traction because it offered higher comfort and lower cost than in-person visits.

Patients referred to physiotherapy typically need to:

Travel to the clinic

Find a parking spot

Wait in line

Do exercises

Go home and repeat several more times

It takes time, effort, and money. The product wasn’t perfect, but it was 10x better than visiting a clinic. Great for patients - but to scale, companies had to drop prices. Patients in the EU weren’t used to paying for healthcare out of pocket. The public system covered most of it. Unit economics suffered, and companies like Omada barely survived before pivoting to B2B.

Why the B2C trap exists:

Broken Unit Economics (CAC > LTV): Acquisition costs on platforms like Facebook were unsustainably high, often exceeding total revenue a user would generate before quitting.

Low Willingness to Pay: Consumers have a “third-party payer” mindset - they believe healthcare should be covered by insurance or employers. Out-of-pocket apps feel like an unfair tax.

The Trust Gap: Patients trust doctors (”White Coats”), not Instagram ads. Without a clinical referral, digital therapies were perceived as low-value “wellness” apps or scams.

The “Cure Paradox”: In B2C, success kills revenue - if the product works and cures the pain, the customer stops paying. In B2B, outcomes drive contract renewals.

Public Healthcare Barrier (EU): In markets with universal healthcare, citizens view treatment as a tax-funded right. B2C medical solutions become niche luxury products with no path to mass scale.

💡 First-movers pay the “Pioneer’s Tax” - the cost of educating the market, navigating regulatory unknowns, and validating product-market fit through expensive failures. Hinge, Kaia, and Omada paid that tax between 2015-2019. Sword watched, learned from their mistakes, and entered in 2020 with a proven playbook and zero education costs. Second-mover advantage in healthcare isn’t about speed - it’s about letting others de-risk the market for you.

But “wait and build” is a high-risk bet, not a safe play. It only works if your technology is actually superior when you finally enter.

Sword leveraged this dynamic by delaying commercial entry. They used the time to refine their technology and build a defensive moat of regulatory approvals and IP:

FDA Class II Medical Device Clearance (2016): Validated Sword as a clinical-grade medical device, not just a wellness app.

CE Mark (~2015-2017): Ensured compliance with European health, safety, and environmental standards.

Additional certifications followed as the company scaled.

The product was neither bad nor perfect. But clinics became gatekeepers - afraid of being replaced. They refused to adopt the technology.

Key reasons:

Clinician Pushback: Physical therapists viewed the technology as inferior to their own hands and 20 years of experience. They saw it as a hassle that disrupted their workflow, not a tool that helped them.

Negative Value: For clinics, the technology meant wasted time and technical frustration. Doctors and therapists refused to use it - and patients, who trust their doctors, never got access to home therapy.

The CEO faced a tough decision: keep developing the product and pivot to B2B - without positive feedback from the professionals who rejected it. Risky and stressful.

The only reasonable path: continue building, collect patient success stories as proof points, and then enter the US market.

💡 By delaying market entry, Sword sidestepped the B2C Trap - but walked into the Provider Trap. Even with FDA Class II clearance in hand, clinicians rejected the technology. Regulatory approval proved the product worked - but couldn’t overcome the politics of threatened professionals protecting their turf.

The real counter-move wasn’t more certifications. It was bypassing the gatekeepers entirely. Sword stopped selling to clinics and started selling around them - directly to employers who cared about outcomes and cost savings, not protecting 20 years of manual therapy experience.

💡 In healthcare, the patient is not the customer - they’re the validation layer. Early users exist to prove clinical efficacy, not to generate revenue. The real money flows from whoever is financially responsible for the patient’s health: employers, insurers, governments. Sword understood this. Their competitors learned it the expensive way.

The “Butterfly” phase

Fundraising

In 2019, Bento spent six months trying to secure a Series A in Europe. He faced nearly 50 rejections - “the kind of no that doesn’t go past the first meeting.”

Reasons for rejection:

Competitor gap: Hinge Health was 3 years ahead with market leadership and “the same solution.”

No traction: Zero US clients and no scalable path in EU clinics either

Geography: A hardware-heavy medical startup based in Portugal.

The critical driver behind US-first strategies for European health-tech founders is the difference in payer incentives.

In the US, healthcare is largely employer-funded (self-insured models). High costs hit the company’s P&L directly, creating urgent demand for cost-containment solutions. Companies have direct financial motivation to adopt efficiency tools.

In Europe, healthcare is publicly funded or state-mandated. The payer is the government or a centralized fund. Sales cycles are bureaucratic and slow. The incentive to optimize is diluted by political and social mandates.

Tech founders followed the money - bypassing Europe’s rigid public systems to attack the US market.

This dynamic also shapes European investors. They either didn’t understand the US employer-payer opportunity, or saw no path through the EU’s public healthcare bureaucracy. Either way - pass.

The turning point: a cold email to Khosla Ventures. Within 4 weeks, the deal was closed - $17M Series A.

The VC choice wasn’t random. Khosla is known for backing high-risk, high-impact bets.

💡 50 European rejections. 4 weeks to close with Khosla. What happened in between matters most. The rejections forced a first principles question: where does the money actually flow in MSK treatment? Not in European clinics, not in B2C patients - but in US employers bleeding $15,000+ per MSK surgery on their own P&L.

The cold email to Khosla wasn’t desperation - it was a calculated pivot to the American VC known for backing high-risk, high-impact bets. Founders finally understood which market their product was actually built for.

💡 Look at the Series E structure: $30M primary capital, $100M secondary. Sword only needed $30M in fresh cash - but investor demand was so high, they facilitated $100M in existing shareholder liquidity.

The signal: the company isn’t burning cash, existing investors wanted to partially exit at $3B, and new investors were fighting to buy in. Textbook pre-IPO positioning - create liquidity for early backers while maintaining growth optionality.

GTM Strategy: Distribution

Omada Health almost died selling MSK treatment directly to patients (B2C) in the US. Kaia Health did better with direct sales in the EU but hit a scaling ceiling. Hinge Health pivoted from B2C to B2B successfully and grew fast, becoming the market leader. Sword copied Hinge’s strategy to enter the US market.

In 2 years, they reached unicorn status (2021).

The model is simple. Sword sells digital MSK programs to companies required to cover employee treatment. Employers are eager to pay because it saves them money. Under US law, employers are responsible for their employees’ medical treatment and rehabilitation.

💡Sword didn’t invent the B2B employer model - Hinge did for the MSK market. Copy the leader’s distribution playbook, win on product. Result: 0 US clients to unicorn status in 24-36 months.

The product was attractive to payers because it wasn’t a nice-to-have wellness perk - it was a cost-reduction tool with measurable medical outcomes, backed by licensed physical therapists, not support staff.

The first principle of this market: companies only buy what saves them money or drives revenue. Sword built everything around this - positioning, pricing, proof. The market got it immediately.

Two pricing mechanics made this work:

First: claims-based pricing - no PMPM fees. Companies pay when they see measurable results and countable savings. Pay for outcomes, not access.

Second: the “godfather offer”. Companies paid X based on estimates, but got a money-back guarantee if Sword didn’t deliver savings. To stay credible, they ran calculations through independent ROI auditors.

This pricing strategy gave Sword a 70% win rate in competitive evaluations. Within 4 years: 10,000+ employer clients across three continents.

Product quality reinforced the strategy. By February 2025, Sword reported 100% client retention. No client has ever left the platform.

Selling to employers was rational. One contract unlocked access to thousands of eligible patients - without selling to each one individually.

💡 Employers already pay claims when employees get sick. Sword didn’t ask them to learn new buying behavior - just redirected that existing budget. They implemented a pay-per-success model with a money-back guarantee (”godfather offer”) and independent ROI audits, removing the last objection. Result: 70% win rate against competitors, 100% retention, 10,000+ clients in 4 years.

Sword recognized early that large enterprise clients (Fortune 500 companies) rarely make healthcare purchasing decisions without guidance from major benefit consulting firms. So they built relationships with brokers and consultants. It’s a grassroots play - local offices, where individual consultants are the real voice behind recommendations.

Unlike competitors, Sword didn’t organize fancy events. They focused on providing brokers with rigorous clinical data and independent ROI audits. They targeted global consulting firms - Mercer, Aon, Willis Towers Watson - which curate vendor lists for HR directors, but built direct relationships with individual consultants.

This strategy reduced “reputation risk” for brokers, making it safe to recommend Sword based on documented evidence.

Sword also partnered directly with Health Plans. This way, Sword becomes an embedded benefit available to the plan’s entire member network. Massive scalability: a single payer contract unlocks access to millions of potential patients without selling to each employer individually.

Selling to employers means winning one battle at a time. Partnering with Health Plans wins the war - embedding Sword into healthcare infrastructure itself.

💡 Two-front distribution attack. Bottom-up: arm brokers with clinical evidence to neutralize their reputational risk - make recommending Sword the safest choice in the room. Top-down: partner with Health Plans to embed Sword into healthcare infrastructure. Selling to employers wins battles one at a time. Health Plan partnerships win the war - one contract unlocks millions of covered lives.

💡 Timing matters. Sword closed Khosla’s $17M in Feb 2020 - the exact month telehealth usage spiked 78x compared to pre-pandemic levels. Lockdowns forced patients to prefer home-based care. Telehealth visits jumped from 14M (2019) to 62M (2020). Physician adoption: from 15% to 86%. Sword didn’t create this wave - but they caught it perfectly. The product was ready when the market suddenly needed it.

Clinical Validation and Outcomes

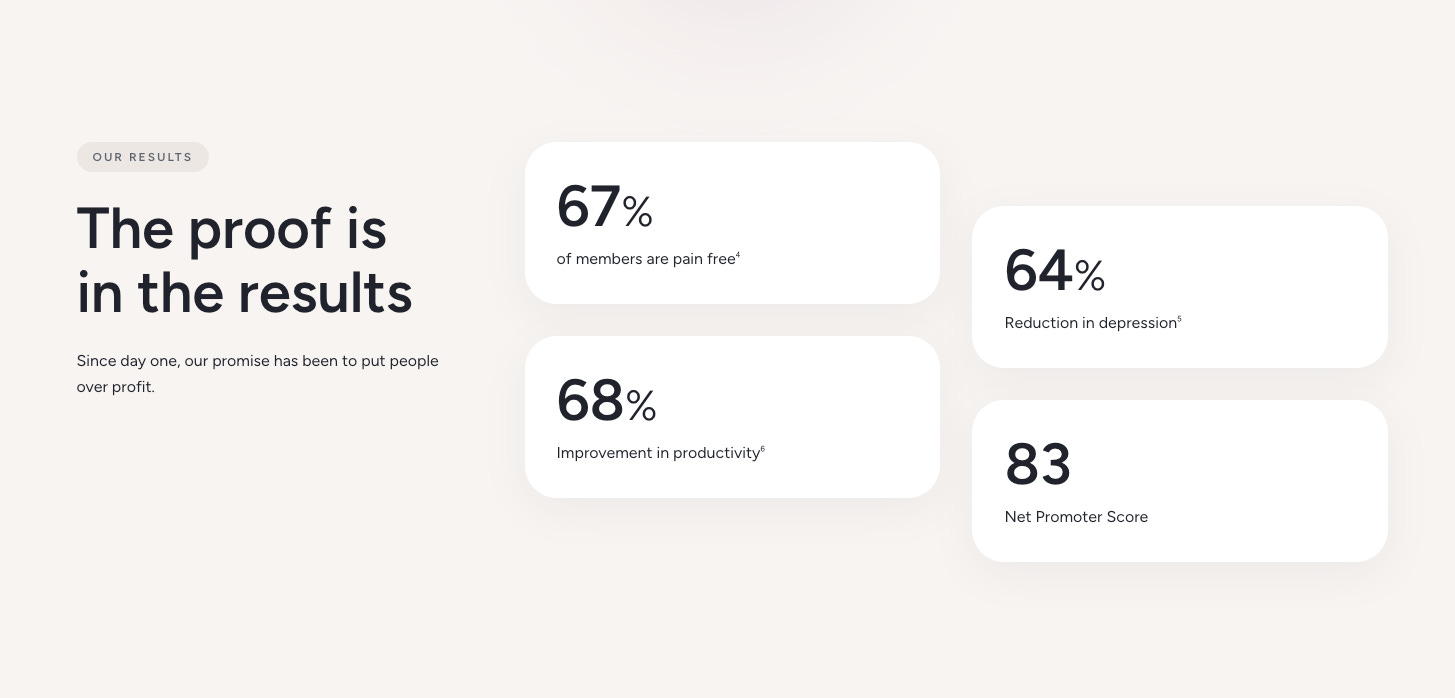

Sword invested heavily in clinical evidence, publishing 43 peer-reviewed papers as of 2025. Key findings from randomized controlled trials:

Efficacy: Digital PT delivers outcomes equivalent to or better than high-intensity in-person physical therapy for chronic low back pain and chronic shoulder pain.

Engagement: 81% completion rate vs. 40-50% for typical in-person PT.

Pain Reduction: 62% reduction in pain scores; 67% of members with moderate-to-severe pain report being pain-free by program end.

Surgery Avoidance: 60-70% reduction in surgery intent; 64% of members become low-risk for surgery.

Productivity: 68% productivity increase worth $2,916 per member per year in recovered workforce value.

Cost Savings: $3,177 saved per engaged member annually on MSK care.

ROI: Independently validated 3.2x1 return on investment; up to 4.4x1 when Predict identifies high-risk members early.

Distribution Channel

In healthcare, distribution is everything - connections, partnerships, sales relationships. Sword didn’t have any of that. So they had to compete with a superior product, “godfather offers,” and innovation.

To maximize distribution, Sword deployed a “Reverse M&A” strategy. They don’t acquire for technology - they believe theirs is already the best. They acquire to “buy the channel”: companies with existing relationships where Sword can inject their product into established contracts.

Acquisitions to date:

In January 2025, Sword acquired Surgery Hero and secured partnerships with 18 NHS trusts in the United Kingdom, serving approximately 10 million patients.

In January 2026, Sword acquired Kaia Health to secure dominance in reimbursed digital MSK care in Europe. Kaia’s exclusive DiGA regulatory approval granted immediate access to 70+ million publicly insured lives in Germany. The deal also absorbed a major competitor with 60+ million covered lives globally and superior computer vision technology requiring no physical hardware. By “buying the channel,” Sword bypassed complex regulatory barriers and established a defensible moat in Europe while consolidating US market dominance.

💡 Most M&A is about technology or talent. Sword’s “Reverse M&A” is about neither - they buy companies for one asset only: distribution relationships.

Kaia acquisition logic: one transaction eliminated a major competitor, absorbed 70M+ covered lives, and bypassed years of German regulatory approval (DiGA). Three strategic wins, one check. This is M&A as market engineering, not empire building.

GTM Strategy: Product Expansion

Sword aggressively expanded into multiple products: Thrive (MSK treatment), Move (injury prevention), Bloom (women’s pelvic health), Predict (AI risk forecasting), and Mind (mental health), Academy (pain education). The goal: shift from “point solution” to comprehensive “platform.”

This strategy was driven by payer expectations, economic efficiency, and the need to maximize ROI.

Large enterprise customers are moving away from point solutions - one vendor for back pain, another for mental health. They prefer platforms that cover multiple conditions. One contract, one provider, everything included.

By offering Thrive, Bloom, and Mind, Sword becomes a one-stop-shop. This increases customer lifetime value, reduces churn risk, and creates barriers for competitors who offer less.

Predict allows Sword to integrate deeply with client medical claims data, making them an essential component of the care continuum - not just an add-on app.

Unit economics improve significantly. Treating multiple conditions per member - back pain and comorbid depression, for example - multiplies value per patient.

The endgame: become the end-to-end operating system for MSK. Own the entire patient journey vertically - from prediction to prevention, through treatment and recovery.

💡 Evolving into a platform was a unit economics optimization move. Initial CAC - hardware shipping and patient onboarding - is a one-time sunk cost. Upselling additional verticals like Bloom incurs near-zero marginal expense. This multiplies Lifetime Value by keeping patients active across the ecosystem, while giving Sword pricing flexibility to structure bundled deals that point-solution competitors mathematically cannot match.

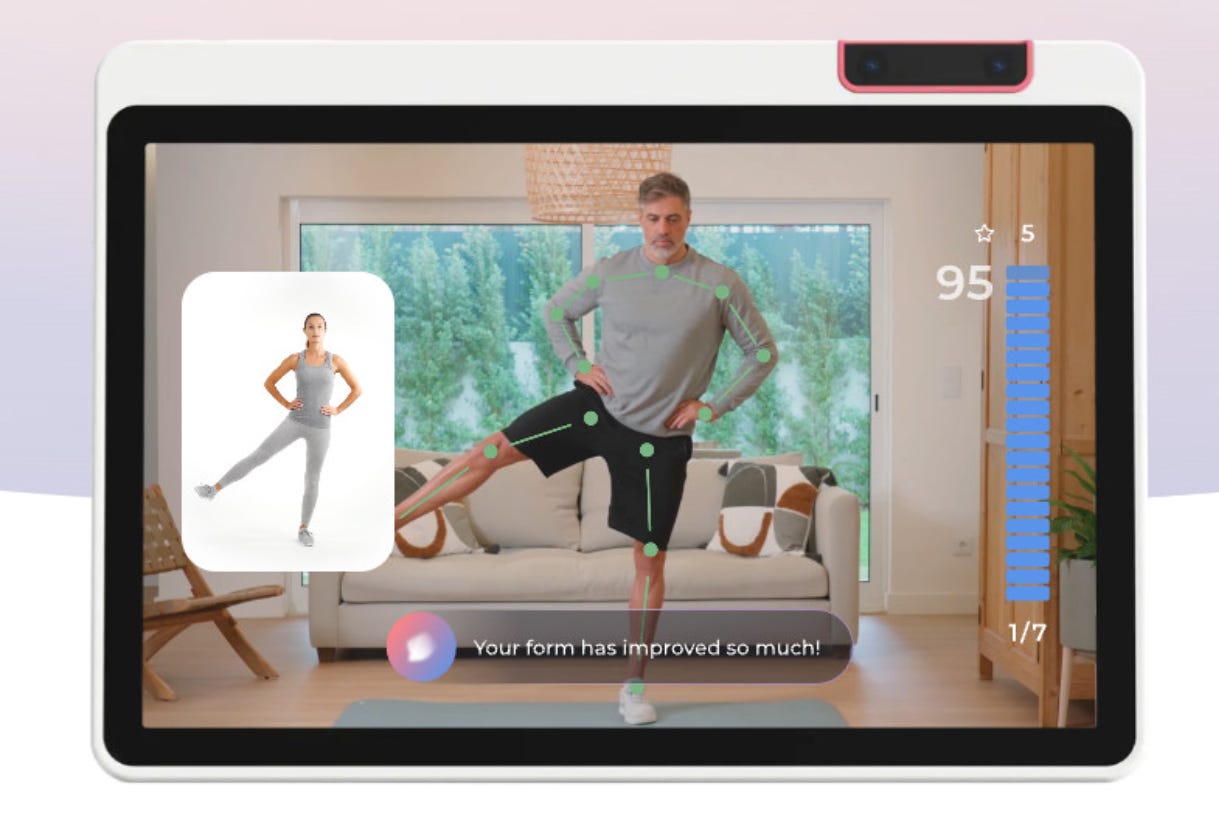

Phoenix

Phoenix launched in June 2024 as the “AI Care Specialist” - a shift from “AI-assisted digital therapy” to “AI-first care.” Unlike Sword’s previous technology, which primarily provided feedback on movement, Phoenix is a conversational interface capable of natural, spoken dialogue. It acts as an always-available therapeutic agent combining real-time monitoring with empathetic interaction.

This fundamentally altered Sword’s unit economics by unlocking massive scalability:

Clinician Efficiency: Therapists can now manage ~700 patients simultaneously - a massive increase from traditional limits.

Staffing Reductions: The shift to AI led to laying off ~17% of therapists in 2024, proving fewer humans can serve more patients.

Structural Cost Advantage: This clinician-to-patient ratio creates a scalable cost structure that labor-intensive models cannot match.

Phoenix also deepened user experience: natural conversation, real-time guidance, full personalization. As a support tool for PTs, it reduces operational costs and drives scalability - especially where clinical supply is a bottleneck.

💡 Phoenix is a revenue engine designed to convert user experience directly into cash flow. By replacing static interfaces with natural conversation, it increases patient engagement - the single most critical metric in a business model where revenue depends on active usage and outcomes.

The efficiency math: traditional PT manages 40-100 active patients. Sword with Phoenix: ~700 per therapist. That’s a 7-17x structural cost advantage. The 17% therapist layoffs in 2024 weren’t downsizing - they were proof the model works.

Nuances and Key Takeaways

A few patterns that built a $4B company:

1. Constraint as advantage EU grant instead of VC. $1M budgets with 12-month kill deadlines. Scarcity forced innovation that well-funded competitors never developed.

2. Follow the money, not the patient First principles question: who actually pays? Not patients, not clinics - employers responsible for employees’ MSK treatment. Every strategic decision flowed from this insight.

3. Speed as moat 15-day client onboarding. 24-month path to unicorn. CTO moved to Chief Strategy Officer because at scale, strategic velocity matters more than technical execution - especially when product-market fit is proven and the market is growing.

4. Institutionalized scarcity They didn’t just talk about cost discipline - they built a system for it. The innovation formula:

Find a General Manager (domain expert)

Give them $1M budget

Set a hard deadline: 12 months

If MVP validates (like Bloom did) → invest more

If it fails to prove itself → kill immediately

This is how you innovate without burning cash on endless R&D.

5. “We’ve just done 5%” mindset Bento repeats this in interviews: mentally, they operate as if they’re still at the beginning. Same philosophy as Bezos’s “Day 1” - the moment you feel established, you start dying. This mental frame keeps a $4B company acting like a hungry startup.

6. Product-centric obsession - the foundation, not the wrapper Most companies are “assemblers” - they combine existing tools, platforms, and skill sets into a service. Deep-tech is different. You can’t build a medical AI from off-the-shelf components. The technology is the business.

In digital health specifically: if clinical efficacy fails, nothing else matters. Sword stayed close to domain experts and treated product development as survival, not iteration.

7. The Evidence Wall Sword systematically converts technological innovation into hard, verifiable assets - legal and scientific. 43 peer-reviewed papers. 37 patents. FDA Class II clearance. CE Mark. DiGA approval.

The power isn’t in any single credential. It’s in the critical mass: an ecosystem of credibility that can’t be challenged in a sales meeting or due diligence process.

Capital can be raised fast. Building this library of clinical and legal proof takes years. Sword used time as an asset, creating a moat that new entrants can’t leapfrog with money alone.

What next?

The “Payvider” Injection Strategy

Sword needs an aggressive move toward European subscription healthcare giants - Bupa (owner of LuxMed), AXA, DKV. Instead of building distribution or doing another acquisition, inject Sword’s technology into the bloodstream of these players.

Current subscription packages from these giants are leaky. Physiotherapy and mental health are treated as afterthoughts - often limited or excluded entirely. This is the perfect gap. Sword doesn’t enter as competition but as a “Plug-and-Play Premium Module” that patches this hole. Bupa alone operates in 190 countries.

The European market is screaming for efficiency. In the UK, private medical insurance (PMI) costs rose 12.6% in 2024. Operators like Bupa and Vitality are desperately seeking technology that reduces treatment costs - not just raises premiums. Sword is the answer.

The fear that Europe is less profitable than the US (where employers pay) is a cognitive bias. The solution: a Hybrid Model that distributes cost burden while protecting unit economics.

1. The Base (Volume): Employer/insurer pays. European markets offer consolidated entry points that the fragmented US market lacks - one partnership with Bupa or DKV unlocks millions, versus selling employer-by-employer in the US.

2. The Savings: Operator pays (e.g., LuxMed/Medicover), giving up margin in exchange for Sword clearing queues from their physical clinics.

3. The Premium (Co-pay): Patient pays. In Europe (especially the Netherlands, where 55% of healthcare spend is private insurance), consumers are conditioned to pay extra for a premium of faster access.

Partnerships with Bupa Group allow Sword to scale while maintaining margins. This isn’t a fight for retail customers. It’s a fight to become the default operating system for European “Payviders”.

The “B2C Silver” Strategy

By 2050, 34% of Europe’s population will be over 60, consuming 70%+ of healthcare spending - mostly on chronic diseases concentrated in seniors. Projected clinician shortage: 1.8 million. The math doesn’t work.

B2C Silver is not the B2C trap. Seniors aren’t working-age patients expecting employers to pay - they’re no longer “productive assets.” Corporations have zero incentive to fund retiree care. The State becomes Payer of Last Resort - and it’s failing.

The Incentive Conflict Public hospitals are a dead end. They get paid when beds are full - preventative technology that keeps seniors home hurts their revenue. States pay for cures (post-fall rehab), not prevention (mobility training).

The Poland Case Poland shows the opening in real-time. NFZ faces a 4.6B PLN budget gap in 2026. 55% of healthcare spending goes to the 60+ population (26% of citizens, projected 40% by 2060). In December 2025, NFZ cut home physiotherapy reimbursements - making human-delivered home rehab economically unviable.

The State admitted it can’t afford human visits in patients’ homes. Sword has no travel time constraints, no staffing limits. When public systems retreat, AI-first care is the only scalable alternative.

The Strategic Maneuver: “Sword Senior”

1. Sell “System Survival,” Not Therapy - The pitch to Government is Capacity Management, not wellness. Hip fracture costs the State up to €2.5k. Sword prevents it for a fraction. Pure arbitrage on public spending.

2. The “Privatized” Wedge - Wealthy seniors (or their children) pay out-of-pocket to escape public system dysfunction (NPS -27%). They’re buying independence from a broken system, not a wellness subscription.r

Public systems are retreating. Demographics guarantee it gets worse. The question isn’t if this market opens - it’s who captures it first.

“We’ve just done 5%.”

Virgílio Bento, CEO Sword Health

Thanks for your time!

Kasper

This piece really made me think! As a Pilates practicer, I often see how important MSK health is. Your analysis on Sword Health avoiding B2C traps and leveraging AI for such massive efficiency gains is truely brilliant. So insightful to see how they cracked distribution and pricing. Amazing to build $4B after 50 rejections!